Buy Now, Pay Later: Smart Hack or Deadly Trap?

05/15/2025

By: Conor Moreau

As prices skyrocket higher and higher, and people struggle to afford things, companies push Buy Now, Pay Later programs to keep customers buying - but are they a smart hack or a deadly trap? Let's dive deep and figure it out together so you can decide if Buy Now, Pay Later is a tool you want to keep in your financial arsenal.

Sooo What is it?

If you've shopped online lately, you've probably seen advertisements for BNPL programs by the time you check out. Every week, it seems like companies are offering another new Buy Now Pay Later program.

They're a nice temptation - I even used them recently for concert tickets. It seemed like an easy choice: get my tickets as soon as possible but pay them off over a few months.

The plans vary, but largely, they all work the same - you buy whatever you're purchasing, but the price is separated into multiple payments, and if you make all the payments on time, you won't accrue any interest or fees.

These payment options are gaining traction due to the lure of no-interest charges, convenient repayment schedules, and easy approvals. Combine these perks with more people relying on credit to make ends meet in an inflated economy, and it's easy to understand the hype. They've become so prevalent that people are even using BNPL for groceries or going out to eat.

Are Credit Cards Not Enough?

BNPL might feel like treading on common ground; it can feel a bit like companies gave credit cards a new coat of paint.

Here's the thing, though: credit card debt continues to skyrocket as people use it as their primary means of payment and as a means to make ends meet. So, when presented with the option of a payment that feels 'risk-free,' users vie for the Buy Now Pay Later option, but the penalties can be even MORE extreme than a high-interest credit card.

They can create a debt cycle that can become almost impossible to escape. Lawmakers looking to protect consumers have called for laws, regulations, and oversight regarding BNPL. Until then, make sure to always read through the terms and conditions!

They WANT You to Fail.

Providers aren't lending out money interest-free out of courtesy or kindness - BNPL only makes a profit from you making mistakes and accidentally missing payments.

They draw you in with a deal that seems amazing, breaking your payments down into equal manageable installments - sort of like layaway programs, but you get the product right away. But what happens when you miss a payment?

Well, that's when they make money. You get hit with SUBSTANTIAL fees and high interest rates.

Financial Weight

Let's imagine BNPL payments like a financial scale. It's easy to see why people are attracted to the interest-free aspect, easy approvals, and simple checkout process, but what happens when it snowballs out of control?

You make a BNPL purchase on the 1st of the Month, and for the next three months, you're making that payment every 1st. No problem, right? That's a small weight on the scale.

Then you make another purchase on the 5th and the 8th, and you use BNPL again. Maybe you even use it through multiple different providers, making it even HARDER to track.

Okay, that's a lot more weight. Now, you're making payments on the 1st, 5th, and 8th for three months. Let's say you add a few more weights to the scale, and suddenly, it's looking really weighed down.

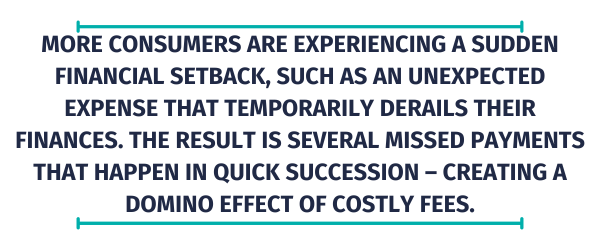

Assuming your paycheck arrives conveniently within these time frames, you might be able to handle the payments (and your regular monthly bills). However, more and more consumers are experiencing a sudden financial setback, such as an unexpected expense that temporarily derails their finances. The result is several missed payments that happen in quick succession – creating a domino effect of costly fees. Late or miss payments can even negatively impact your credit score!

With Great Power Comes Great Responsibility

If you decide to use these BNPL payment options, use these tips to help ensure your finances aren't negatively impacted.

- Limit Use: Keep your BNPL payments to a minimum and only for purchases that justify spreading out the payments over time. Forego using BNPL on frivolous expenses.

- Automate Payments: Enrolling in automatic payments with the BNPL provider is the best way to prevent missing payments and incurring costly fees. Make sure you have the funds available before your due date to avoid overdrawing your checking account.

- Track Your Due Dates: Use an app or calendar to log each of your upcoming payments. This tactic is especially helpful if you're using multiple BNPL lenders, as it provides an easier way to see all your upcoming payments in a single place.

We're Here to Help!

Convenience often comes at a hidden cost we don't consider. If you're going to use BNPL while checking out, make sure you keep track of your payments and avoid financial challenges.

If you have questions about BNPL payments or want to consolidate these payments into a lower-rate personal loan, we're happy to help. Please stop by any of our convenient branch locations or call 800-834-0432 to speak with a team member today.

Stay up to date and join our email list.

The Atlantic blog strives to deliver informative, relevant, and sometimes fun financial information. If you enjoyed this article, please forward it to a friend.

Each individual’s financial situation is unique and readers are encouraged to contact the Credit Union when seeking financial advice on the products and services discussed. This article is for educational purposes only; the authors assume no legal responsibility for the completeness or accuracy of the contents.