Class is in; it's Time to Learn HELOC Fundamentals.

08/21/2025

By: Conor Moreau

We all want our own space. As a person who grew up in a family of six, I still drool at the idea of a spacious home that's all MINE. When you own a home, it's truly yours to decorate, remodel, and make a reflection of your ideal life.

It also provides you with the ability to build equity or value from your property. Equity that can help you achieve your financial goals.

Home equity lines of credit (HELOC) provide homeowners with an affordable financing option that can be used for just about anything – home remodels, vacations, higher education, and debt consolidation. For some, these loans can be confusing due to their terminology and features.

Pull out your notebook, take a seat - class is in session, and until the bell rings, we're going to break down how HELOCs work.

Uh, How Do I Use My Home's Equity?

We're diving right into the deep end. This is where you'll want to get the calculator out or start doing some math on your paper.

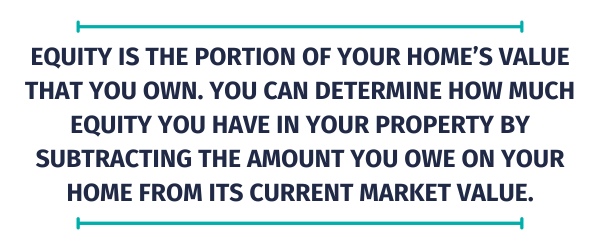

Equity is the portion of your home’s value that you own. You can determine how much equity you have in your property by subtracting the amount you owe on your home from its current market value.

Home Equity = Home’s Current Market Value – Amount Owed (Mortgage Balance)

For example, assume your home is worth $450,000, and you still owe $300,000 on your mortgage. In this scenario, your equity would be $150,000. You can borrow a portion of this equity through a home equity loan.

The two most popular home equity loans are:

- Home Equity Loan: A traditional home equity loan is a closed-end loan where all the funds you borrow are provided upfront in a single lump sum. The interest rates are typically fixed. Then, you repay the loan with set monthly payments – just like a car loan.

- Home Equity Line of Credit (HELOC): A HELOC is a revolving line of credit that functions more like a credit card. Homeowners are given a credit limit or maximum amount they can borrow. Then, they can borrow as much as they need whenever they need it during the draw period – as long as they don’t exceed their credit limit.

HELOCs provide homeowners with unmatched flexibility and affordability. It’s even EASIER with Digital Banking at Atlantic, which lets you transfer money from your HELOC directly into your checking account.

POP QUIZ: How HELOCs Work.

So, you opened a HELOC. What now? Well, your lender provides you with a credit limit or the maximum amount you can borrow against your property/home's worth. Once the amount has been established, you can withdraw from it whenever you want during the draw period.

Upon making a withdrawal, your monthly payments begin. As you make payments, those funds become available to borrow again throughout your draw period.

Assume you open a HELOC for $50,000 with the Atlantic. Initially, you borrow $10,000 with $40,000 still available to borrow. You will begin making monthly payments on the $10,000 portion.

Now, assume you pay down $2,000 of the $10,000 borrowed. You will now owe $8,000, with $42,000 available to borrow from your credit limit.

This process will continue throughout your HELOC’s draw period.

Wait, What is a Draw Period?

Unlike traditional home equity loans that distribute all the funds upfront as a lump sum, HELOCs provide more flexibility. While you’re approved for a set borrowing limit, you only have to borrow (and pay interest on) what you need – when you need it.

HELOCs are divided into two parts: the draw period and the repayment period.

- Draw Period: The “draw period” is the timeframe when you can borrow from your approved credit limit. While HELOCs function similarly to credit cards, they don’t last forever like a credit card. You’ll have a set time when you can borrow funds, typically between 5 and 10 years.

- Repayment Period: The “repayment period” begins immediately after the draw period ends. You can no longer borrow funds from your approved credit limit. Any outstanding balance on your HELOC will be converted into monthly payments to repay during the remaining loan term.

Repayment periods generally match the draw period in terms of timeframe.

Not sure what you would use a HELOC for? Check out our Financial Tips to Do Better: The 7 Best Ways to Utilize Your Home's Equity

TLDR:

Owning a home allows you to build equity, which can help meet financial goals. A Home Equity Line of Credit (HELOC) offers flexible and affordable financing, functioning like a credit card with a set credit limit. You borrow what you need during the draw period, repay, and can reborrow the funds. HELOCs can fund remodels, education, or debt consolidation.

We’re Here to Help!

Accessing your home’s equity is a significant financial perk for homeowners. With lower rates, longer terms, and borrowing flexibility, HELOCs provide an affordable means to achieve financial goals and cover unexpected expenses like medical bills. By understanding how HELOCs function, you’ll be better equipped to put all the perks to work for you.

If you want to learn more about home equity loans and lines of credit, we’re happy to help. Please stop by any of our convenient branch locations or call 800-834-0432 to speak with a team member today.

Stay up to date and join our email list.

The Atlantic Financial Tips to Do Better strives to deliver informative, relevant, and sometimes fun financial information. If you enjoyed this article, please forward it to a friend.

Each individual's financial situation is unique, and readers are encouraged to contact the Credit Union when seeking financial advice on the products and services discussed. This article is for educational purposes only; the authors assume no legal responsibility for the completeness or accuracy of the contents.